Central European investment volumes exceed €6 billion in 2011

According to global property consultant Cushman & Wakefield, investment activity in Central Europe grew substantially in 2011, with €6.1 billion invested in the core markets of Poland, Czech, Slovakia, Hungary and Romania. This is more than double the €2.9 billion invested in Central Europe during 2010.

Poland continues to lead the region, but Czech experienced the largest increase in transaction volumes year on year, increasing from €479 million in 2010 to €2.2 billion in 2011. Poland remained in front with €2.58 billion transacted in 2011. Hungarian investment volumes increased from €240 million to €728 million, Romania edged forward with volumes increasing from €241 million to €320 million, whilst €263 million was transacted in Slovakia in 2011, up from €53 million in the previous year.

“The strong performance in the Czech and Slovak markets in 2011 reflects the improving perception of those markets amongst international investors and the continuing growth in the number of domestic investors. This provides an excellent platform for another strong year in 2012. There are some major transactions in the pipeline that could result in a similar volume being completed in 2012 as the previous 12 months. We also expect additional new sources of capital to enter the market,” says James Chapman, head of Capital Markets, C&W Czech Republic and Slovakia.

Transaction volumes in Central Europe had been expected to exceed €6 billion in 2011 following a strong performance in Q1 and especially Q3, however, momentum was lost in Q4 as investors assessed the market turmoil that returned to the Eurozone, and bank lending slowed.

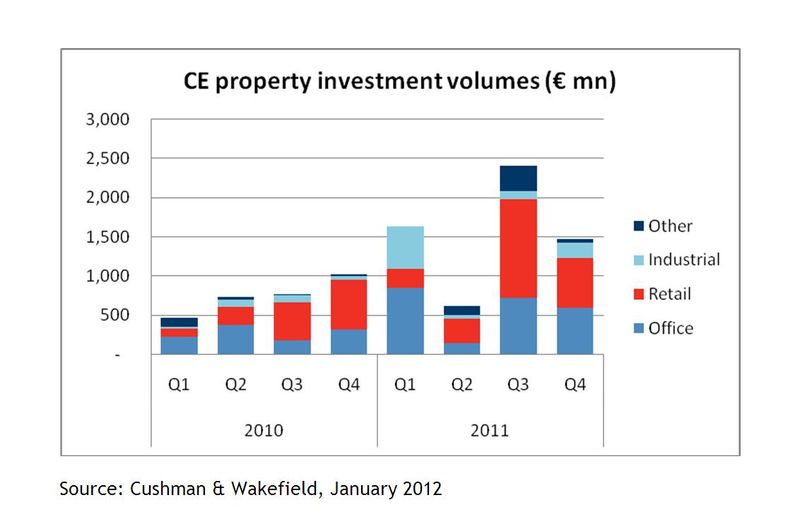

Investor’s sector preferences in 2011 remained largely unchanged on the previous year. Investment into retail continued to dominate, although the proportion fell back from 49% in 2010 to 40% in 2011. Office investment remained constant at 37%, and investment into the industrial sector increased from 8% to 15% in 2011.

“Retail investment in the Czech market (51%) was ahead of the CE average and it was an exceptional year for industrial investment (23%) led by the two major VGP transactions. Offices (26%) were significantly behind the CE average but we expect this to change in 2012 with a major increase in the volume of office deals,” says James Chapman.

Whilst there was general agreement that Poland had achieved the status of a core market in 2011, not all investors were seeking safe havens, and a strong appetite for value prevailed with some investors priced out of Poland and won over by the relatively more attractive pricing in Czech.

International buyers accounted for 76 % of the volume transacted in the Czech Republic. The share of domestic investment was 24 % (€ 544 million). CPI was the most active domestic investor.

Commenting the outlook on the core CE markets for 2012, Charles Taylor, Partner at Cushman & Wakefield said;. Given the more difficult financing environment, we don’t expect 2012 volumes to match the previous years; our forecast is around € 5 billion”.

Source: Cushman & Wakefield

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook