After five-year increase there is decrease in building shopping centres

It would seem, that customers’ attitudes and moods did not manage to change substantially during the elapsed year. People, if we do not take new unemployed ones into consideration, did not cease from their sense for spending; among inhabitants of neighbour states shopping tourism starts growing up even. Everything (maybe excluding goods of long-term consumption or real estates sharply dropping in prices) still remains the object of everyday, immediate and spontaneous interest, without speculatively motivated waiting or calculated discretions. But from the most recent study – the European Shopping Centre Development, worked out by the estate consulting company Cushman & Wakefield, results that not negligible part – up to 7 millions m2 of planned new shopping centres delay, suspend or is terminated due to the crisis.

Simply told, prognostics were wrong. Reality of their broad-minded forecast from July 2008 for year 2009 withered by 40 percentages to 10 millions m2, whereas another drop is expected in year 2010 – to totally 7 millions m2 of area. If this amount is confirmed, the lowest volume of shopping centre expansion since year 2005 and finish of the five-year lasted mounting of their development in the same time is concerned by Cushman & Wakefield (C&W).

Europe: a pause like a chance to establish itself

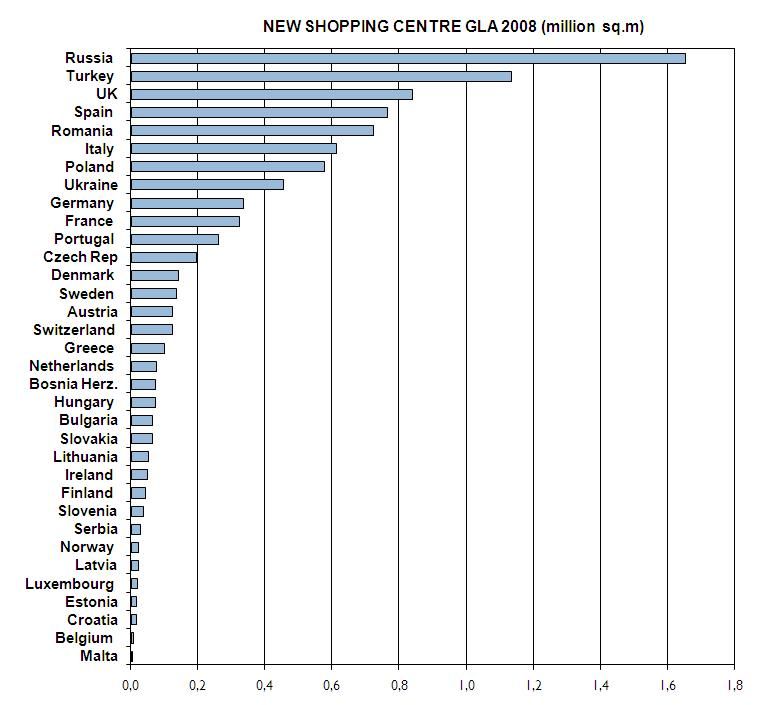

European cannot complain of the record-making year

2005 at all. 310 shopping centres were opened or enlarged starting with Russia

(1.65 millions m2), following with Turkish, Great Britain and Romania with

a gap.

European cannot complain of the record-making year

2005 at all. 310 shopping centres were opened or enlarged starting with Russia

(1.65 millions m2), following with Turkish, Great Britain and Romania with

a gap.

Either way, expectations for next years 2009 and 2010 got substantially more realistic mainly thanks the combination of several factors according to the study by C&W (the economy crisis deepening, making conditions of financing more restrictive, lower trustworthiness of developers). It means that all developing markets (Russia, Ukraine and Turkish to some extent) will be affected by the crisis, what is also confirmed by estimations of the new building-up for next years, decreased from 58 to 22 percentages since last year.

Alexander Colpaert from the C&W European department of market investigation is persuaded, on the other hand, that deceleration of building needs does not mean automatically negative trend for developing European countries, because some localities (for example capitals) registered booming in new shopping centres last years in a relatively short time period. „Actual environment is giving time to developers, businessmen and local administration to analyse the current situation and possibility to assess eventual impact of further building-up of new shopping centres. By this way the present pause will offer opportunity to existing shopping centres to establish themselves on the local retail markets,“ Colpaert thinks.

Slovakia: deceleration will bring stronger stability

Situation in Slovakia does not look pessimistic seemly. Practically every month news are coming about some shopping centre either being prepared or being built, which slowly become a matter of course in regional metropolis from the east to the west border of the state (Bratislava, Trnava, Nitra, Trenčín, Žilina, Zvolen, Banská Bystrica, Poprad, Košice, Prešov). However the entire trend looks a bit differently.

„Momentarily we are witnesses of the market

deceleration in shopping centres chains in Slovakia. However, for existing

shopping centres it can be positive, because it will mean for them stronger

stability yet. In localities, where we registered the need for shopping centres,

we expect, that developers will find the way, how to produce a strong product,

which will be useful for both parties, retailers and local population as well.

Developers, who fulfil criteria, have still opportunity to obtain finances from

some banks, the most often for projects with the good concept in the best

locality and which will accept retailers in spite of the market deceleration in

order to feel that also in case of long-term indebtedness they can be

successful,” Andrew Thompson, the executive director and the chief of offices

and capital market department for Cushman & Wakefield in

Slovakia, told.

„Momentarily we are witnesses of the market

deceleration in shopping centres chains in Slovakia. However, for existing

shopping centres it can be positive, because it will mean for them stronger

stability yet. In localities, where we registered the need for shopping centres,

we expect, that developers will find the way, how to produce a strong product,

which will be useful for both parties, retailers and local population as well.

Developers, who fulfil criteria, have still opportunity to obtain finances from

some banks, the most often for projects with the good concept in the best

locality and which will accept retailers in spite of the market deceleration in

order to feel that also in case of long-term indebtedness they can be

successful,” Andrew Thompson, the executive director and the chief of offices

and capital market department for Cushman & Wakefield in

Slovakia, told.

In spite of that the deceleration in retail is still lower than in administrative or in industry and demand for retail objects still outlasts steadily according to the March investigation of CB Richard Ellis Company. From the most current – yesterday CBRE report results that, the rental space of shopping centres achieved 720 400 m2 in Slovakia in the first quarter of this year, what is almost double compared with year 2005.

The biggest 40-percentage ratio has Bratislava today. In year 2009 about 115 000 m2 of retail spaces, 32 % at Nitra, 30 % in Bratislava and 23 % at Trenčín hereof ought to be created. „These numbers indicate gradual concentration of retail outside the capital. However, regarding the outlasting crisis, we expect that finalization of some projects will delay,“ the fresh CBRE report says.

Czech: the will of banks will be tested out in years 2010 and 2011

Czech reality is a bit more moderate compared with the European one – from totally planned 250 thousand m2 of new and enlarging existing centres only about 150 thousand m2 were realized in fact. Less or more, the total area of the retail segment achieved together reputable 1.95 millions m2 in Czech republic. Prognoses for year 2009 are almost closely the same.

„The plans on new shopping centres building-up achieved substantial changes this year. The most recent intentions of developers speak about the building-up of 150 thousand m2 of new spaces including enlarging existing projects. One year ago the volume by approximately 65 percentages higher was considered yet – almost 250 thousand m2 of new spaces in 15 shopping centres. We register projects involving the area of 380 thousand m2 for year 2010, but financing these projects is ambiguous today,“ Martin Žížala, the chief of the C&W retail spaces department in Prague, discovers. However, the will of banks to finance new shopping centres will be tested by projects planned for years 2010 to 2011, with reference to Alexander Rafajlovič, the chief of the market investigation department. „Developers, who thought about this year opening really seriously would not have problems to do it, because they ensured financing the projects before the crisis burst out yet,“ he adds.

Graf: European states according to m2 of new shopping centres in year 2008

Definitions of terms and their specification

Shopping centre: According to the ICSC (International Council of Shopping Centres) definition the traditional shopping centre upon Slovak conditions is considered the real estate serving for retail, operated like one unit involving the entire rental space larger than 5 thousand m2 and with 10 independent entities minimally. So if a shopping centre is spoken about, combination of a shopping gallery and a main renter is considered in principle – in the form of a hypermarket or a larger supermarket the most often.

Retail park: The development including three or more shopping units in the frame of one object involving the entire area about 5 thousand m2 or more is concerned. The counterpart of those projects is always a parking place shared by all operators in the frame of the park. A retail park is usually built-up by one developer in unique design. The classical example is Avion Shopping Park in Bratislava. One type of shopping concept, which reminds retail parks, is a cluster – a group of minimally three separately staying units placed in close vicinity. Each of them can have different owner. A counterpart of it is parking places – either common or separate for particular operators. The commercial zones near IKEA in Bratislava or Tesco, Lidl, Terno, Carrefour in Petržalka can serve like examples.

| The planned building-up of shopping centres – gross rental space in m2 (2009 – 2010) | ||

|---|---|---|

| Country | m2 | Growth % |

| 1. Turkish | 2 003 343 | 42.8 |

| 2. Rusia | 1 251 866 | 16.1 |

| 3. France | 1 400 000 | 8.1 |

| 4. Poland | 1 193 600 | 19.7 |

| 5. Italy | 1 192 399 | 10.1 |

| 6. Spanish | 1 042 753 | 10.6 |

| 7. Romania | 882 193 | 47.1 |

| 8. Germany | 686 003 | 5.0 |

| 9. Bulgaria | 660 786 | 450 |

| 10. Netherlands | 632 000 | 11.1 |

| 14. Czech | 540 520 | 28,5 |

| 15. Slovakia | 520 566 | 70.6 |

| New shopping centres in year 2008 – gross rental space in m2 (01/2008 – 12/2008) | ||

|---|---|---|

| Country | m2 | Growth % |

| 1. Russia | 1 653 103 | 23.4 |

| 2. Turkish | 1 134 603 | 32 |

| 3. Britain | 838 455 | 5.6 |

| 4. Spanish | 764 564 | 8,5 |

| 5. Romania | 721 342 | 62.6 |

| 6. Italy | 613 532 | 5.5 |

| 7. Poland | 575 440 | 10.5 |

| 8. Ucraine | 455.664 | 28,7 |

| 9. Germany | 335 919 | 2.7 |

| 10. France | 323 111 | 2,1 |

| 12. Czech | 194 838 | 11.5 |

| 22. Slovakia | 62 890 | - |

Illustration photo – Europa Passage Hamburg, GUM Moscow Tables, graphs, definitions – source Cushman & Wakefield

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook