Logistics and storage spaces: the moment of inertia weakens

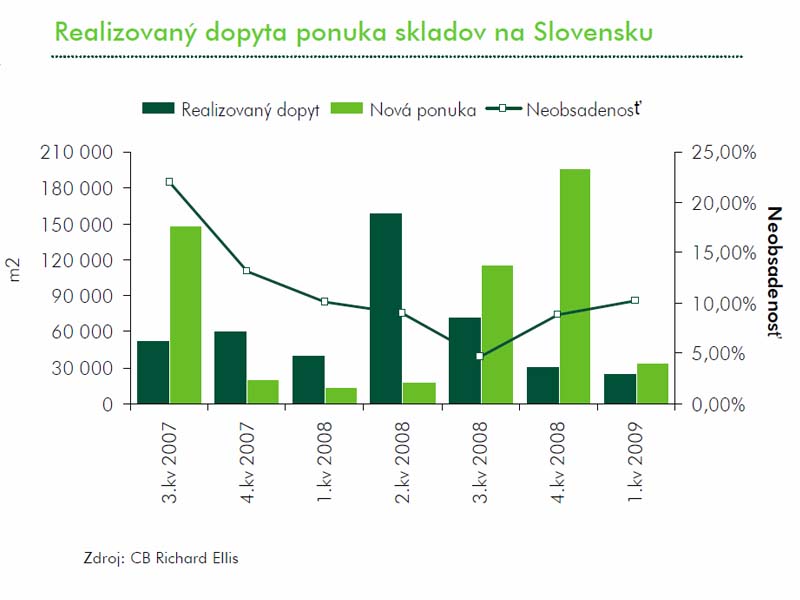

Surveys of consulting companies show that although the beginning of 2009 looked promisingly from the perspective of many macroeconomic and real indicators, it only related to the statistic compared to the same period of 2008 or 2007. The moment of inertia induced by the point-blank of the previous economic growth, however, slowly but surely weakens and when compared semi-monthly and semi-quarterly the first notable consequences of the global crisis impact come forward in local conditions. CB Richard Ellis Company confirmed it in the latest issue of BIG BOX – a periodic report on the market with industrial, logistics and storage real estates. The results for the first quarter of 2009 say: the total volume of leased logistics spaces achieved 25 176 m2, what means the semi-quarter decrease in realized demand by 19 percent!

What really creates the uniqueness of storage and logistics market? This is mainly the speed of new premises construction, but also the preparedness of building lands for the requirements of demand. According to the BIG BOX report the realized demand for logistics and storage spaces achieved the record level in 2008. For the first quarter 2009, its volume, however, created only 35 percentages from the last year's average quarter value.

A significant decrease in new projects

CBRE noted totally 5 leases in the first quarter,

while the average size of one was 5 035 m2. Interesting and symptomatic is that

all these transactions were realized exclusively in the Bratislava region (the

Greater Bratislava Area), what represents 72 percentage increase in the

whole-Slovakia proportion compared to the same period in 2008. „Noteworthy is

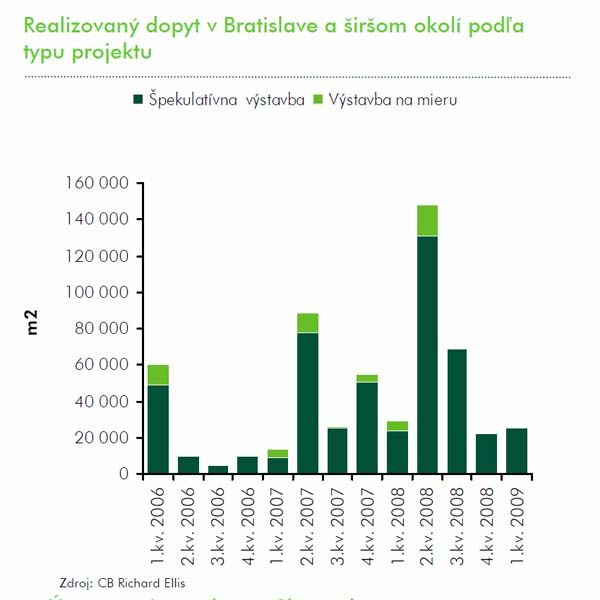

the fact that all the newly leased spaces were built speculatively this quarter

and were not pre-leased,“ says the CBRE report.

CBRE noted totally 5 leases in the first quarter,

while the average size of one was 5 035 m2. Interesting and symptomatic is that

all these transactions were realized exclusively in the Bratislava region (the

Greater Bratislava Area), what represents 72 percentage increase in the

whole-Slovakia proportion compared to the same period in 2008. „Noteworthy is

the fact that all the newly leased spaces were built speculatively this quarter

and were not pre-leased,“ says the CBRE report.

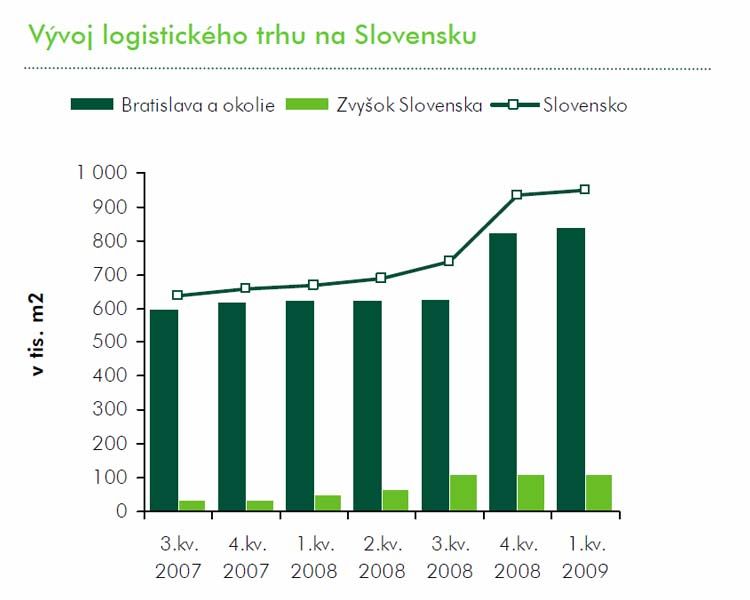

The area of modern storage spaces in Slovakia achieved the value of 950 295 m2. Approximately 88 percentages of them (838 278 m2) is located in the Bratislava region, the biggest proportion of which along the D1 and D2 motorways and only 112 000 m2 outside the Greater Bratislava Area. Similarly, the volume of 34 200 m2 of newly created logistics spaces, which enhanced the domestic market from January to March 2009, is while suggesting an annual increase by 140 percentages, but compared to the last quarter of 2008 at the same time signals up to 83 percentages fall!

The head of CBRE Industrial Parks department, Peter Jánoši, attributed the significant decline in being prepared and realized projects by their more difficult financing but also a caution of the developers themselves. Also their final users are not behaving differently, according to his opinion. „With an uncertain future, some of them postponed or suspended their plans to indefinitely,“ explains Jánoši.

Rents on an historical minimums

At the end of this year first quarter the volume of

spaces in construction fell by app 42% – to about 46 950 m2 (significant

semi-year decrease by 76%) compared with the last quarter. From the total area

of logistics premises in construction (31 600 m2, of which 15 350 in the Great

Bratislava Area) 19 percentages create pre-leased spaces and up to

81 percentages of speculative ones (Profinal: Logistics Centre

Bratislava-Ivanka, VGP: storage spaces at Malacky). On the side of demand

unfinished projects created only one fifth compared to 2008.

At the end of this year first quarter the volume of

spaces in construction fell by app 42% – to about 46 950 m2 (significant

semi-year decrease by 76%) compared with the last quarter. From the total area

of logistics premises in construction (31 600 m2, of which 15 350 in the Great

Bratislava Area) 19 percentages create pre-leased spaces and up to

81 percentages of speculative ones (Profinal: Logistics Centre

Bratislava-Ivanka, VGP: storage spaces at Malacky). On the side of demand

unfinished projects created only one fifth compared to 2008.

As seen from the Graph 1, ProLogis with 40-percent share of the total volume of spaces, followed by the great distance of J & T IIG (13%), AIG Lincoln (12%), HB Reavis (11%), Karimpol and Otners (after 7%), Pinnacle (6%) and Goodman International (4%), remains the dominant developer on the market with logistics and storage real estates in the first quarter.

As regards the new offer, the biggest brought the

logistics Park of ProLogis Company at Galanta (79%) and the Profinal Company

supplied remaining 21% to the market. The amount of leases in the best

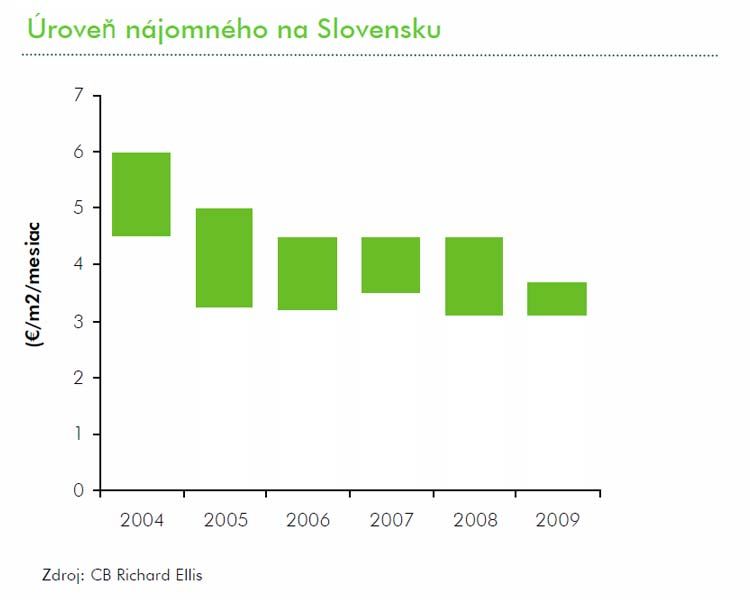

Bratislava spaces maintained stability and currently ranges from 3.40 to

4.00 € / m2 / month – depending on the locality and occurrence of

competitors eventually.

As regards the new offer, the biggest brought the

logistics Park of ProLogis Company at Galanta (79%) and the Profinal Company

supplied remaining 21% to the market. The amount of leases in the best

Bratislava spaces maintained stability and currently ranges from 3.40 to

4.00 € / m2 / month – depending on the locality and occurrence of

competitors eventually.

On the other hand, the pressure on banks or other funding bodies and the relatively high non-occupancy of already existing projects depressed rents in some locations to historical minimums, "warns Peter Jánoši in the BIG BOX report for the increased rate of incentives, by effecting of which the amount of rents decreases.

Will bank restrictions support leases?

„We expect that a large part of the lands prepared for construction of logistics premises will remain unused, till the demand for storage spaces is not increased and the non-occupancy rate is not reduced, "says the BIG BOX report. Continuing restrictions in the bank financing of the construction of logistics and storage spaces will support pre-negotiated leases and will slow construction. In the context of the overall tension in the economy the availability of leased spaces and individually negotiated terms will predetermine length of leases.

In the coming months, CBRE assumes the growing

importance of tailor-made projects and leases, as a direct result of the

optimization of costs and narrowing of states of some companies, not only in the

administration but also in the logistics sectors. It can be concluded that the

trend of slowing down leases, which has resulted to the increasing of the rate

of non-occupancy of logistics premises to the current 10.25% (semi-quarter

increase by 1.43 basis points), will turn soon? Guarantee for any answer for

these questions no one can give in this moment.

In the coming months, CBRE assumes the growing

importance of tailor-made projects and leases, as a direct result of the

optimization of costs and narrowing of states of some companies, not only in the

administration but also in the logistics sectors. It can be concluded that the

trend of slowing down leases, which has resulted to the increasing of the rate

of non-occupancy of logistics premises to the current 10.25% (semi-quarter

increase by 1.43 basis points), will turn soon? Guarantee for any answer for

these questions no one can give in this moment.

Definitions according to CBRE

Storage spaces – modern storage spaces, Class-A, developer projects

Non-occupancy rate – the ratio of free storage spaces and the total volume of

stores

Realized demand – the net storage space leased for a certain period

Premises in construction – developers’ storage spaces in construction

Graphs and data – resource CBRE

Graph 1 – The share of developers in the Slovak market by size of storage

spaces for the 1st quarter 2009

Graph 2 – The volume of leases (realized demand), the new offer of stores and

the rate of their non-occupancy

Graph 3 – Development of the logistics market in Slovakia Graph 4

– Realized demand in the Great Bratislava Area by the type of project

(speculative or tailor-made construction)

Graph 5 – The level of rents in Slovakia

Jagg.cz

Jagg.cz Linkuj.cz

Linkuj.cz Google Bookmarks

Google Bookmarks Live bookmarks

Live bookmarks Digg

Digg Del.icio.us

Del.icio.us MySpace

MySpace Facebook

Facebook